Welcome back to the Roadmap to Financial Health! If you are new to the Roadmap, we recommend starting at Step 0.

You’ve developed your goals and logged into your new budget tracking tool, you’ve linked your accounts, and now you’re really ready to begin. You need to build a budget that accurately reflects your spending power and needs. A budget that takes into account all the places your money sneaks off too, so you don’t have to scramble when that once or twice a year expense comes up.

You’ve developed your goals and logged into your new budget tracking tool, you’ve linked your accounts, and now you’re really ready to begin. You need to build a budget that accurately reflects your spending power and needs. A budget that takes into account all the places your money sneaks off too, so you don’t have to scramble when that once or twice a year expense comes up.

This post will help you set up an initial budget and get you started but do not lock this down as the be all and end all of your budget for the year. Expenses you forgot to account for in the first round will come up, goals and priorities may change, you may just go through way more toilet paper than you thought. Revisit your budget categories and limits at least once a month and check in on your progress to your goals. After this setup, the subsequent processes will be faster, but not any less important. With that said, let’s dive right in.

If you want to download a PDF of this guide, along with a spreadsheet to set up your budget, you can download the Better Budget Toolkit here!

Table of Contents

How to Build a Budget that Actually Works

The titles of all your steps, which are pretty self-explanatory, are right here. Down below, I give details on thinking about each step, so you start budgeting in a smart and thoughtful way. You can use this post as a walkthrough to follow as you build your budget. I highly recommend reading the details, but if you feel you’re an experienced budgeter who already has a good handle on their finances, you can probably just skim the headings.

I use certain high-level groupings for budget categories that I think help prioritize spending and allocation of income. In most budgeting tools you can customize your master categories so set the names of those titles first. If you use a service like Mint.com that doesn’t easily break down into groupings, I would recommend writing out your budget in the groupings first to help set your mind to what your spending priorities are.

Note: I highly recommend You Need a Budget for tracking your budget long-term. But for new budgeters, sketching your expenses out on paper first is a helpful exercise and makes filling out your YNAB budget less overwhelming.

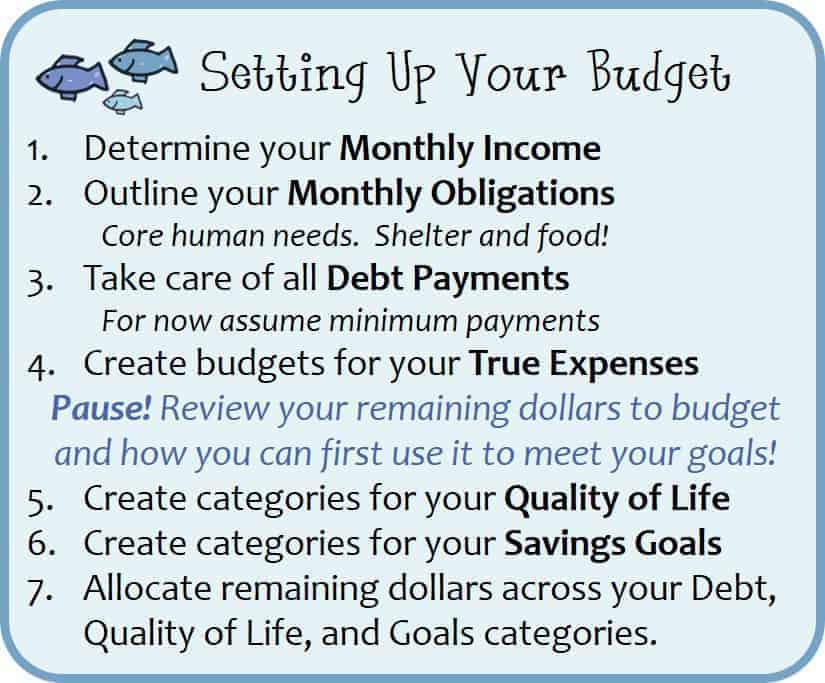

Determine Your Monthly Income

This step is possibly the easiest, as your most likely sources of income are just your and your spouse’s salary. There are only three comments I will make here:

- Do not estimate your income or calculate based on gross income. Pull up your most recent pay stub or look at your last month’s direct deposits.

- Bi-weekly and weekly pay schedules: If you get paid bi-weekly, two months out of the year you get three paychecks instead of two. If you get paid weekly, four months out of the year you get five paychecks instead of four.

- Base your budget on two monthly paychecks or four weekly paychecks and those “extra” checks you get each year will put you ahead of the game on saving for your goals.

- Include any monthly inflows. If you receive EBT or WIC support, have income from a side job, rental property, or any other financial support make sure your budget includes it. This only works if none of your money is “free” from budgeting. We are putting every dollar to work!

- For EBT and WIC support (food stamps), put the available funds right into the budget categories they are used for.

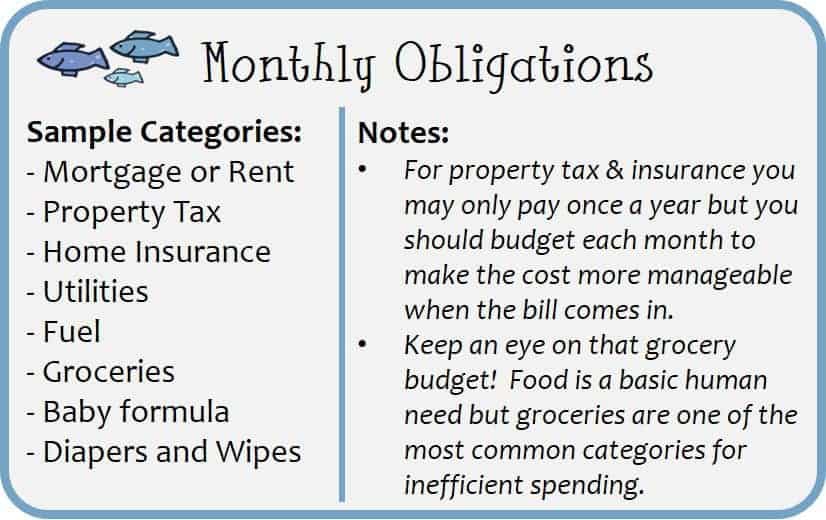

Outline Your Monthly Obligations

The first thing your income needs to tackle is your basic human needs. No, not your need for those adorable throw pillows at Target or that new video game, your needs like shelter and food. These expenses keep the lights on, and you have to account for them every single month.

Once you know your Monthly Obligations and the cost, subtract the total from Monthly Income and move to the next step.

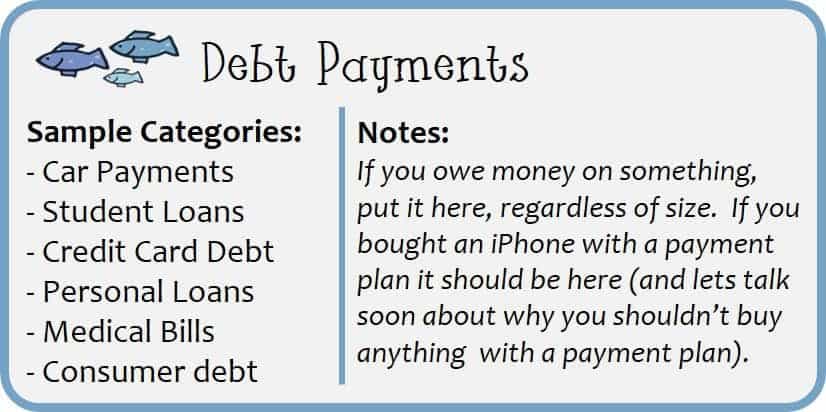

Take Care of All Debt Payments

If you don’t have debt, do a little jig and move on to the next step. If you do have debt, it may be why you’re here. Paying off debt is no fun. You are paying for things that already happened which means that a good chunk of the money you work hard to earn every month is just gone. Poof. No enjoyment.

In this step, we are just covering your minimum payment requirement for all non-mortgage debt. This is an important step for two key reasons. First, it reminds you that taking on debt moves covering that debt over all the things you enjoy, you put a roof over your head and food on the table, and then you pay your creditors. This is the only way to get out of debt. Second, it shows you in a cold, hard total number how much of your income is going to debt every month. This fact is your get angry, get motived, driving force to get yourself out of debt.

All too often, we convince ourselves that the new phone is “worth” $19 a month, or that we work hard and deserve that plush, new couch. These decisions may feel good in the moment, but you are sacrificing your financial sanity for the future. Is that new phone going to feel worth it 15 months in when you still have ten months of payments?

Once you know the carrying cost of your debt, subtract the total from what was remaining after your Monthly Obligations and move to the next step.

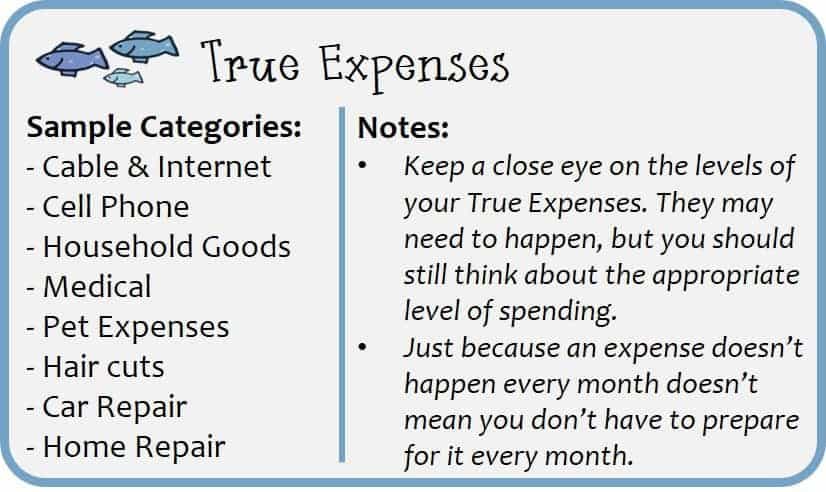

Create Budgets for your True Expenses

We all know that in the 21st century the demands on your spending go far beyond your basic human needs. You can’t function without your cell phone, the kids manage to go through forty-three million rolls of toilet paper, the roof leaks, and the dog needs to eat. True expenses are things that just need to happen. It doesn’t mean you aren’t spending too much on those things – cable & internet and luxury spa haircuts being prime examples – but you have to allocate some money to it.

One note on True Expenses: Anything truly discretionary does not belong here. Gym memberships, eating out budgets, hobbies, and things like it will be addressed in Quality of Life.

If you own a car or are responsible for the maintenance of your home, car and home repair should get some budgeted money every single month. Have you ever had your car break down and the mechanic come out to tell you, “Good news! I can fix your problem for $15!” No? Me neither. But if you save a little every month for that eventual disaster, even if it’s just $10 a month towards an oil change, you won’t need to panic when the worst happens.

PAUSE!

Congratulations! You’ve reached the point in your budget where you’ve covered your necessities, and you get to decide how to make your remaining money best work for you. You can put more money towards paying down debt, start setting aside gift money for the holidays or give your family a budget to have a weekly meal at a restaurant. This is the fun part. But before you set off to put all remaining money towards luxuries, let’s talk about three key things.

- Emergency fund: Step 2 on the roadmap to financial security, empowerment, and sanity is growing your emergency fund. There will be a whole post on this soon, but as a rule of thumb you should aim to have $1,000 in an emergency fund if you still have debt, and build to 3-6 months of emergency savings once you no longer have debt.

- Pay down debt: This is Step 3 on the roadmap and is a fairly obvious one, but if you still have debt, you should keep your Quality of Life allotments as low as possible (without making you feel totally constricted) and pay down debt.

- Save for retirement: You guessed it! Saving for retirement is Step 4 on the roadmap. The rule of thumb is to save at least 10% of your pre-tax income towards retirement. This means if you make $50,000 a year, $5,000 a year needs to go into a retirement fund.

If your emergency fund isn’t healthy, you still have outstanding debt, and you are below your target for saving for retirement make sure to allocate as little money to Quality of Life categories as you can feel comfortable doing and pursue those three measures of financial health.

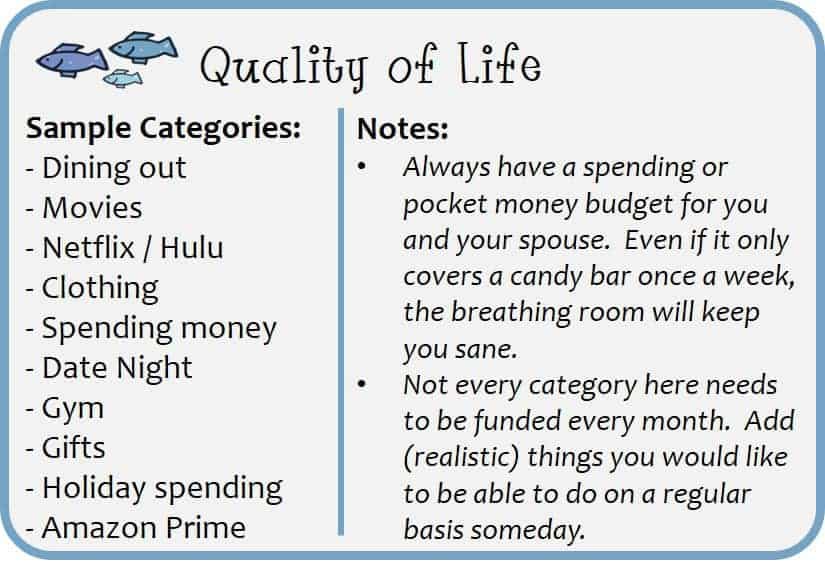

Create Categories for Your Quality of Life

This step is a little different than the early ones because we aren’t allocating money to the categories yet, just adding all the other little categories we spend money on to our budget tracker or making a list by hand. This master grouping includes the really fun things like eating at restaurants, new clothes and spending money; and some planning things like a budget for holiday gifts and setting aside money for annual subscriptions like Amazon Prime. If you spend money on it on a semi-regular basis and it hasn’t been included so far, make sure it fits in a category here.

Create categories for your Goals

If you read my first post and completed Step 0 (find it here), you have already created your goals so you could budget with a purpose! Now write them down in a way you can actively allocate money to them. Do you want to build a $1000 emergency fund? Save for a trip to Disney? Buy a new bike? Put these long-term goals under the Savings Goals master group.

Note that if your goal is to pay down debt, you will add money to your debt payment section from the beginning with what you have to allocate from your discretionary spending (Income – Monthly Obligations – Minimum Debt Payments – True Expenses).

Allocate your discretionary income

When you hit PAUSE! halfway through this process, there was a certain amount of money you had left over that we will call your discretionary spending (Income – Monthly Obligations – Minimum Debt Payments – True Expenses). Now that you have all your remaining categories for Quality of Life and Savings Goals set up think about how you want to allocate those discretionary dollars. If you are in a relationship, this should be a discussion, so you are on the same page and working towards financial health together.

If you’re in debt, can you make a pact with your spouse to eat at home for a whole month, and put that $150-$200 you typically spend at restaurants toward your credit card debt. But also consider whether you are more likely to stick with it if you give yourselves $50 for one night out in the middle of the month. What are you comfortable spending on your kids and family at the holidays and what does that mean you need to save each month to do so without pulling out the credit cards in December?

This part is entirely up to you and the speed you want to achieve your goals. The only job you have here is to allocate every single dollar. Put every discretionary dollar to work so you know that $50 you set aside for a pizza night mid-month is really the amount, and you don’t have a slush fund to dip into.

And now you are off to the races. Excellent job powering through, having tough discussions with your spouse, and setting a budget that works for you. Hopefully, this is the longest amount of time you will have to spend thinking about your budget for the near future. Checking in once or twice a week to see how your spending is going and adjusting your budget parameters if need be should only take 10-15 minutes from now on. Pat yourself on the back, you have taken the first major step towards financial health!

How have you set up your budget in the past? What worked and what didn’t? Let me know!

Read the next step on the Roadmap to Financial Health here: Step 2 – Grow Your Emergency Fund.

Love it. With the graphics, you actually make it look fun. 😉

It really doesn’t have to be painful! 🙂

This is a really great thorough goal! After my husband and I budget for our necessities, and savings we budget personal personal spending for us individually. It’s been a great system for us!

Budgeting personal spending is huge! You need to have some wiggle room in your budget to not feel completely constrained.

Thanks so much for reading and sharing your system!

Love the graphics! Great tips! Budgets are so boring to me but it has to be done. Thanks for the tips!

Hah, budgets are never going to be a day at Disney, but totally agree that they are necessary. At least you know the more thoughtfully you set it up the first time, the less headache it will be in the future. Thanks for reading!

The was one of the most detailed budgeting post I have read and I love it!! This will really help get me back on track!! Thank you!!

Thanks Leah! So glad I could be helpful. Good luck getting your budget on track!

I really need to stick to a budget. I had a cushion when I quit my job in January to become a freelancer but that cushion is dwindling as months are so unpredictable and bills have to be paid.

Congratulations on committing to freelancing full time! I am sure it feels a bit stressful to be losing some of your cushion, but maybe a budget can keep you in a good place. Good luck building your freelancing career! Thanks for reading 🙂

Great post! We always need help with budgeting!

Thanks for reading! Budgeting is definitely a practice of continuing improvement and adjustment. Always good to keep looking for ways to tweak to focus more on your goals.

Ugh! I wish I could get organized like this. My husband and I are terrible with budget, but he is a picture guy… Maybe I’ll have him take a look at this and finally get on a plan!

The visuals help!! Maybe try sketching it out together instead of focusing just on the numbers. Good luck!

This is something that my husband and I continually work towards. We are slowly getting our finances in check and we love it!

Such a good exercise to go through! And i love the quick version in the graphics next to the detailed text 🙂

This is a very good article. I live by a budget. When I first started working with a budget I quickly learned I needed a spending journal. The reason for the need of a spending journal was I really didn’t have a good idea of where my money was going. Since than I still use the spending journal because I am able to quickly find waste. Money that would have been wasted is now saved for something I really need or really want. The spending journal has been a real money saver for me.