Why does the average investor see significantly lower returns than the investment funds they use? Why can’t we stop ourselves from buying high and selling low? Basically, why can’t we get out of our own way and reach our financial goals? This gap in results is precisely what Carl Richards tackles in his easy-to-read book, The Behavior Gap.

This book review is the first of the five I promised in mypersonal finance summer reading list. It was a perfect fun, summer read and a great place to start! It also kicks off my monthly personal finance book review series. You can see all of my completed book reviewshere.

Table of Contents

The Behavior Gap by Carl Richards – Book Review

Overall Rating: (4.0/5.0)

Who it is for:

This book is for anyone who has ever acted on a cocktail stock tip or wanted to panic and buy/sell their investments after watching the morning news. This book is a simple read for those who want to learn about how our emotions can impact our investments, particularly our long-term returns!

Clocking in at just 173 pages with lots of charts, this book took me barely two hours to read (a couple of days of train commutes). This makes it an excellent choice for people who want to be a little more aware of the emotional potholes that can trip up their investments, but who also don’t want to read a tome of boring investment terms.

What I liked:

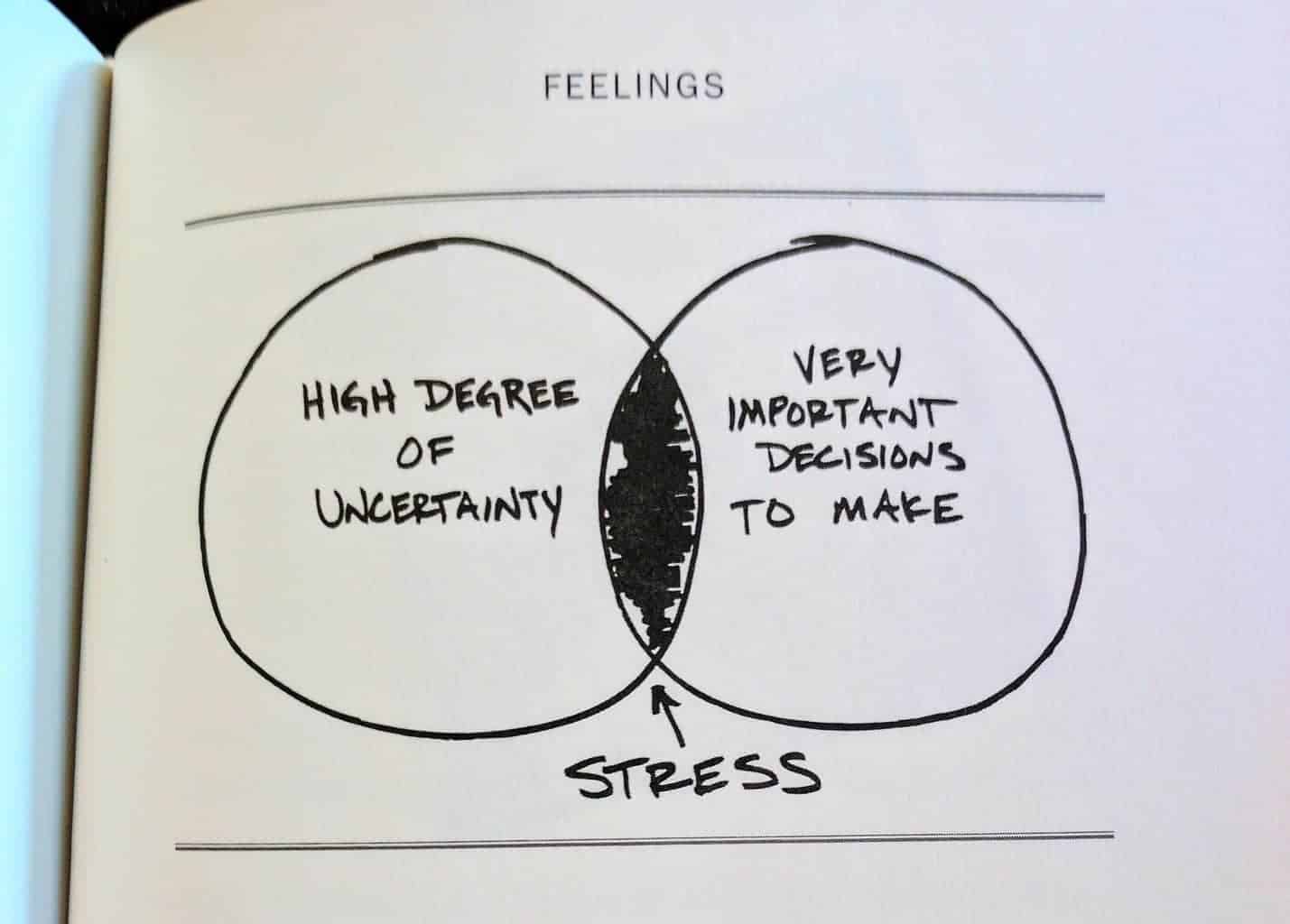

The Behavior Gap does an excellent job outlining how our behavior impacts our ability to build wealth and reach our goals, with zero confusing jargon or condescending tones. Carl Richards makes explaining the basic failings of human beings when it comes to investing fun and easy to understand. And the Sharpie napkin charts speak volumes.

My favorite takeaway in the book was the importance of simplicity. A complicated set of budgeting and investment strategies will only cloud your ability to determine if what you are doing is working, and makes it more likely you throw in the towel before you’ve really had a chance to make a positive difference in your net worth. Keep it simple!

What I didn’t like:

If you’re looking for a book to help you determine a financial plan for your family, this isn’t it. You won’t get an answer on what to do with your money; you’ll get insight on how to handle your emotions! It doesn’t dive into what investment tools (like low-cost mutual funds) can really help you, and doesn’t walk you through a method of building a simple financial plan for your family.

On some levels, I think this makes sense. Richards was aiming to write an easy-to-read book without complicated jargon. Diving into products and trying to outline what works for what situations would have added a lot of mess. Maybe that is covered in his other book, The One-Page Financial Plan!

Where to Buy: You can purchase The Behavior Gap on Amazon, here!

Main Takeaways in The Behavior Gap

The Behavior Gap is all about simplicity and making more careful, conscious decisions in our planning processes to give us a sound basis on which to make future choices. Things change, and our plans will never be perfect, but a well thought out plan will allow for small course corrections instead of massive changes in strategy. It will also give you a base on which to test your emotional decisions. In other words, “Am I doing this because I’m scared or am I doing this because something has actually changed?”

Below, I’ve picked some of my favorite lines from the book and how they impacted my main takeaways from The Behavior Gap.

Risk is what’s left when you think you’ve thought of everything.

Behavior Gap, pg. 127

I loved this line and copied it into my notebook as soon as I read it. (Yes, I still carry a small paper notebook and pen!) There is a tendency for new investors to think any investment plan needs to cover every possible scenario. They have heard the horror stories of people losing their whole retirement in the stock market, and they want to reduce their risk. Totally understandable. But not really helpful.

The thing is, investing always includes risk. Adding complication to your plan doesn’t reduce risk, it just increases your stress. It creates more moving pieces for you to worry about and when something inevitably goes wrong, you’re likely to try to alter your whole strategy to cover that one risk instead of recognizing it as what it is – probably a short-term bump in the road.

The simpler you allow your investment plan to be, the greater understanding you can have of how it works. This increased understanding will help you stay the course through the tough times. You’ll have more faith in the long-term outcome of your system and fewer assumptions to question.

Remember that you have zero control over what the market does and at least some control over what you do. The next time life starts to feel too complex and out of control, remember that you can get recentered by focusing on the simple (note: I didn’t say easy) things you can do to impact your personal economy.

The market will go up, down, and sideways during your investment horizon. Unfortunately, there is nothing you can do to control it and no pundit or “expert” can tell you where it’s headed. What you can do, is focus on what you can control. Invest in a skill to increase your earnings power. Adjust your budget to allow you to save and invest a little more and move you closer to your goals. Take on a new project at work to move you towards your next promotion. Focus on you, invest according to your plan, and the rest will follow

This quote is spot-on with my thoughts on how to handle a market downturn. In my opinion, a downturn is a perfect time to put your blinders on and focus on something you can do to improve yourself! Take a break from the news and staring at your 401(k) balance. There is nothing you can do to force it to go up and moving to cash will only lock in your losses.

Trying to predict the future makes us anxious. Anxiety can make us poor.

When it comes to investing, we all want someone to tell us the secret. It is why many people continue to trust overconfident financial advisors who say they can protect them from losses or predict the next downturn. It is why we place value on loud headlines about potential market crashes and TV shows covering the stock you need to “Buy, buy, buy!”

However, investing is a game of imperfect information. The global market is driven by way too many interconnecting moving pieces to allow anyone to see the whole picture and predict the future consistently. The investing greats, such as Warren Buffett, John Bogle, and Ray Dalio, understand that restriction. We need to as well.

Set your plan based on what you know about yourself and your goals, and ignore the small pieces of information about the supposed direction of the market or potential for Amazon to take over the world with delivery drones and robots. Don’t try to predict the future. Have respect for the fact that uncertainty is alright and that you don’t have to be able to understand all the moving pieces (or react to any individual one) to reach your long-term goals.

Slow and steady capital is short-term boring. But it’s long-term exciting.

What more is there to say? Spending responsibly, saving consistently, and relying on diversified, low-cost mutual fund investments may not be sexy to talk about at the annual holiday party, but it will get you where you need to go!

Have you read The Behavior Gap by Carl Richards? Did you enjoy it? What did you learn from the book? Let me know in the comments!

How's Your Money Health?

Wondering whether you’re doing the right things with money or what you should focus on next? Download our quick financial health checklist and see where you stand!

I read this book recently ? I thought it was good but it was a bit of a review. I did like the pictures and how simple he made it as I am more of a visual person.

Who it is for:

Who it is for:

I read this book recently ? I thought it was good but it was a bit of a review. I did like the pictures and how simple he made it as I am more of a visual person.